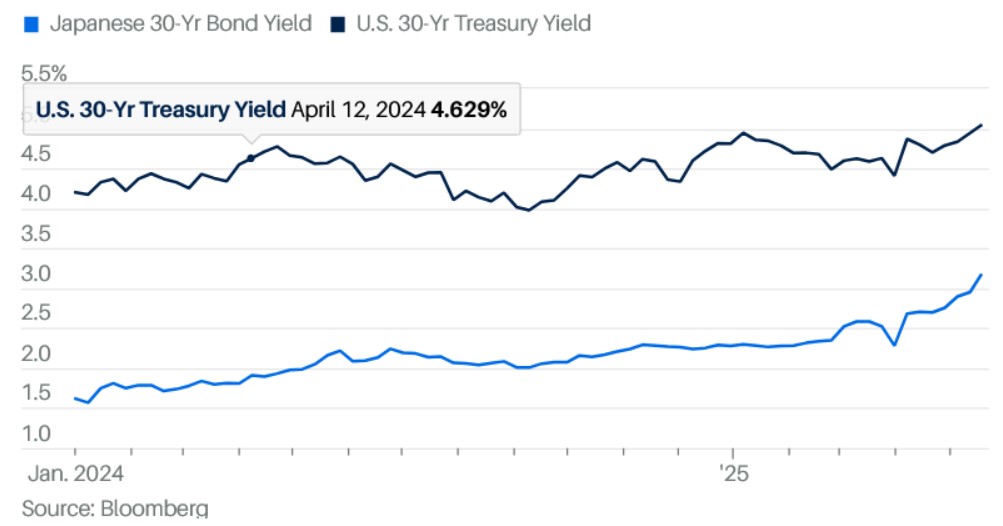

As the world witnesses a sharp rise in long-term interest rates, attention is turning to a phenomenon that began in Japan and may soon ripple through global markets. Yields on 30-year Japanese government bonds have surged past 3%, prompting Japanese investors to repatriate their funds instead of investing in U.S. Treasuries.

The chart shows that although the yield on the 30-year U.S. Treasury has climbed above 5%, once currency hedging costs are factored in, it becomes less attractive than Japanese bonds. This shift in yield dynamics could drain substantial liquidity from U.S. and European markets, especially from Japanese investors who have long relied on higher returns abroad through the so-called “carry trade.”

But the impact doesn’t stop with Japan. The rising yields reflect mounting pressure from deteriorating fiscal conditions in major economies—chief among them the United States, which is grappling with a fiscal deficit exceeding 6% of GDP and a projected public debt trajectory reaching 120% within a decade. The situation worsened recently with Congress’s approval of the “Big Beautiful Bill,” which includes massive tax cuts expected to further inflate debt burdens.

In this context, the cost of long-term borrowing is rising, putting pressure on equity valuations and increasing the risk of a market downturn. The narrowing gap between stock returns and Treasury yields is also weakening investors’ appetite for risk.

Today, global markets resemble a ship weighed down by debt, heading toward a stormy vortex—and the winds from Japan were the first warning signs. As yields climb and enthusiasm for foreign assets wanes, fears are growing of broader disruptions that could shake the financial system. The question remains: will the rest of the markets recognize the threat before the storm hits?